Medicare isn’t quite giving you the coverage you need, and you’re wondering if there’s another option. You may have heard of Medicare Advantage and Medigap, but what exactly are they? And perhaps more importantly, what’s the difference between them?

The first question is easy to answer. In short, Medicare Advantage and Medigap are both collections of health insurance plans available to recipients of Medicare. These plans are designed and offered up by private insurance companies and approved by Medicare and/or the Department of Insurance.

The second question is not so easy to answer. The best way to describe the differences in Medicare Advantage vs. Medigap is:

- A Medicare Advantage plan provides all of the basics of Medicare along with some additional benefits. A Medicare Advantage plan will combine the coverage received from Part A and Part B of Original Medicare.

- A Medigap plan is used in combination with Medicare. It supplements Medicare coverage with some more benefits. With Medigap, you will keep Original Medicare and use those benefits along with your Medigap coverage.

Put simply, Medicare Advantage offers many advantages that regular Medicare may not. And Medigap fills in some of the coverage “gaps” left by Medicare. You cannot have a Medicare Advantage and a Medigap plan at the same time and, in fact, it’s illegal for an insurance company to sell you both.

There are many more subtle differences between Medicare Advantage and Medigap. In this article, we’re going to dissect those differences.

Because of the differences, and because each person has different medical needs and budgets, it’s important to fully understand the aspects of both Medicare Advantage and Medigap before making any purchases.

The Basics of Medicare

Before diving into Medicare Advantage vs. Medigap, let’s first outline some basic information about Medicare. To understand Medicare Advantage and Medigap, you must first understand the four different parts of Medicare.

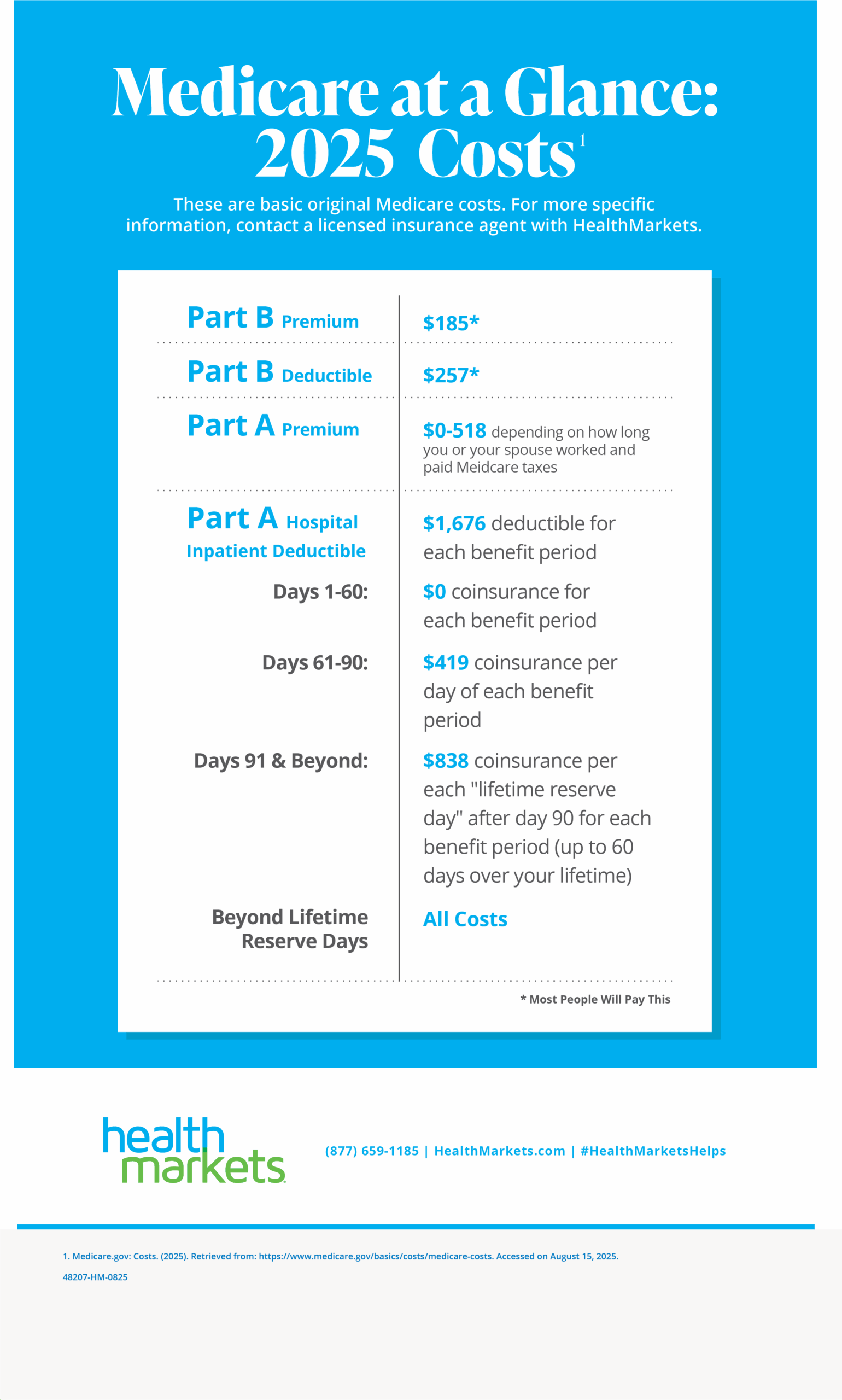

Medicare Part A is your hospital coverage. Medicare Part A covers hospital stays, nursing care and even some home health services and hospice care. When you enroll in Social Security, you are automatically enrolled in Part A.

Medicare Part B is medical coverage. This part pays for a portion of your doctor visits, medical equipment, outpatient procedures and care, x-rays, lab tests, mental health treatment and ambulance services. Medicare Part B is optional. However, you may pay a higher premium if you did not enroll during the Initial Enrollment Period. The combination of Part A and Part B is known as “Original Medicare.”

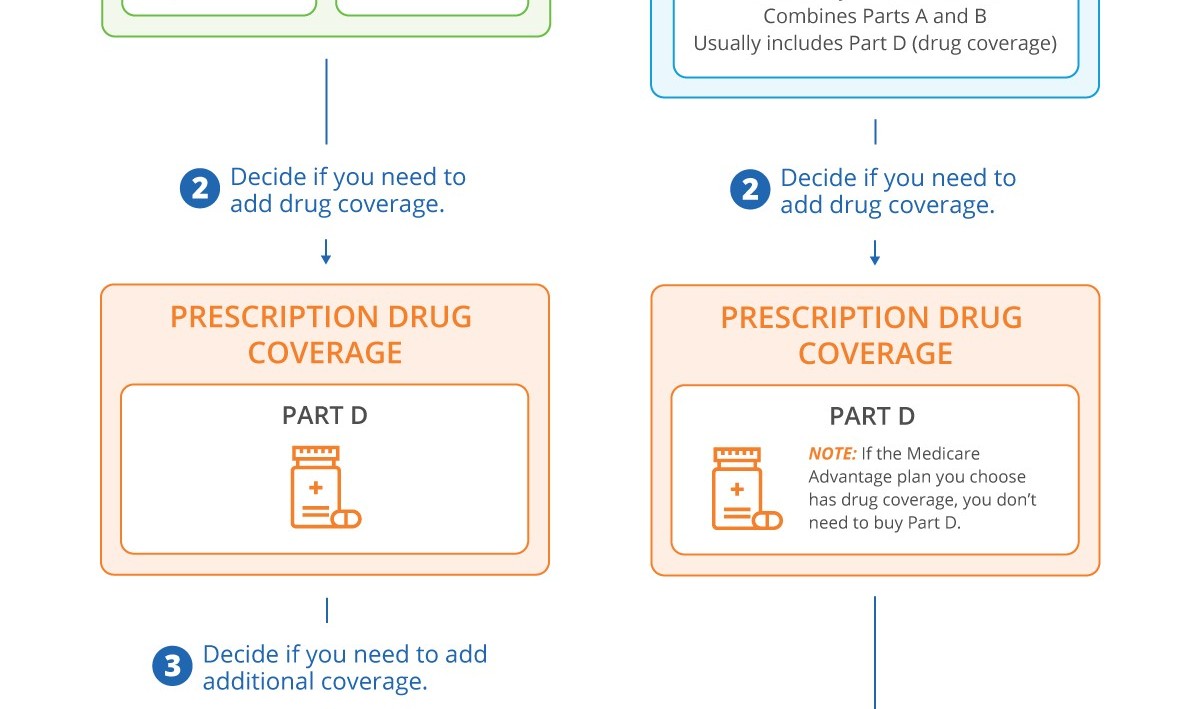

Medicare Part C is what’s known as Medicare Advantage. Medicare Advantage is a collection of plans offered by private insurance companies and approved by Medicare. It provides you with all the benefits that are included in Part A and Part B of Original Medicare.

Medicare Part D is a prescription drug plan. Part D is also optional and is only available to those enrolled in either Part A or Part B. Like Medicare Advantage, Part D plans are offered through private insurance companies and approved by Medicare.

Medicare Advantage

In order to purchase a Medicare Advantage plan, you must first be enrolled in both Part A and Part B. By law, Medicare Advantage plans must cover the same services as Original Medicare. But Medicare Advantage plans al

so include some extra benefits not covered by Original Medicare. Depending on the plan, these extras can include coverage such as vision, dental or prescription drugs.

In addition to offering different coverage options, Medicare Advantage plans may also come with some alternative payment terms and restrictions to Original Medicare.

Just as with traditional health insurance plans, Medicare Advantage plans come in the forms of HMO (Health Maintenance Organizations), PPO (Preferred Provider Organizations) and POS (Point of Service).

There are also Special Needs Plans (SNP), which are designed for people with specific diseases, and Medical Savings Account Plans (MSA), which combine a high-deductible plan with a bank account where Medicare deposits money.

In total, there were 1,945 Medicare Advantage plans available on the market in 2015.

Medigap

Unlike Medicare Advantage, Medigap is not one of the four parts of Medicare. But similar to Medicare Advantage, you must first be enrolled in Original Medicare in order to enroll in a Medigap plan.

The intention of Medigap plans, also called Medicare Supplement plans, is not to provide more coverage in addition to what Medicare covers, such as vision, dental, eyeglasses or hearing aids. Instead, the focus is on covering the out-of-pocket costs, or gaps, left by Medicare, such as copayments, coinsurance and deductibles.

There are 10 different types of Medigap plans, each identified by a letter. The table below illustrates the coverage makeup of each plan.