A Consumer’s Guide to Health Insurance in Florida

If you’re seeking individual or family health insurance in Florida, let us show you the options available to you before you purchase a plan. But first, here’s some quick facts about Florida health insurance:

- 1.9 million Floridians signed up for plans on the Affordable Care Act (ACA) exchange in 2020.1

- In 2010, before the enactment of the ACA, Florida’s uninsured rate was 21.3%. In 2019, it dropped to 13.2%.2

How Do I Get Health Insurance in Florida?

If you do not have Florida health insurance benefits through an employer, you have options for where you can purchase health coverage:

- An online shopping site such as HealthMarkets

- A licensed agent in person or over the phone, also available from HealthMarkets

- The federal government’s insurance exchange

- Directly from an insurance company

- State-funded programs for low-income residents

When You Can Buy Florida ACA Health Insurance

If you are a U.S. citizen living in the state, you can purchase a Florida Affordable Care Act plan during the Open Enrollment Period,3 which runs from November 1 through December 15.4

But, there is some flexibility when you can enroll depending on certain circumstances. You can enroll in a plan anytime if you have a “qualifying event,” which includes but is not limited to:5

- Getting married or divorced

- Having a baby or adopting a child

- Losing health coverage

- Relocation

- Becoming a U.S. citizen

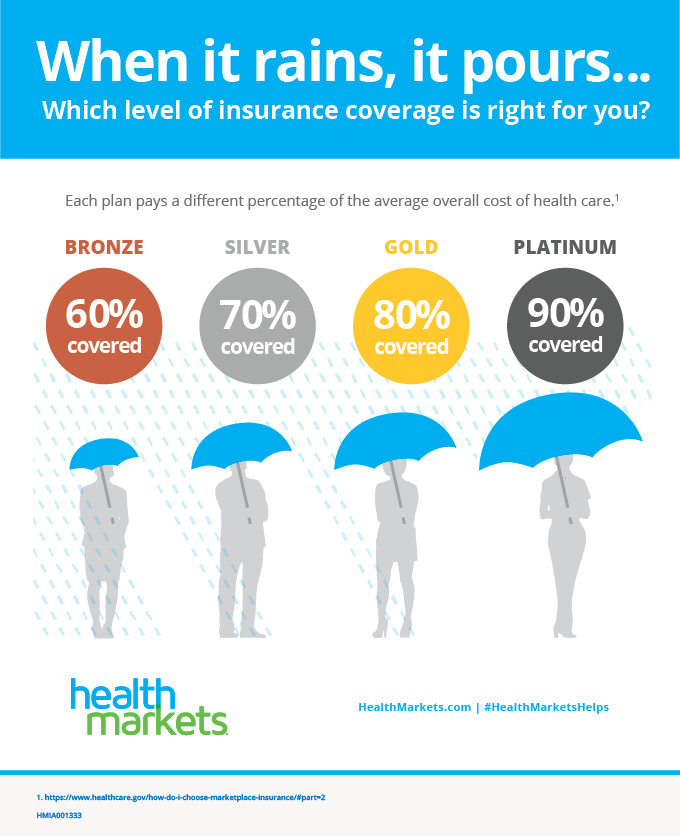

Types of ACA Plans6

There are four main levels of ACA plans available: platinum, gold, silver, and bronze. These plan levels, often called “metal levels,” vary based on the percentage of out-of-pocket costs you are responsible for paying after you’ve met your deductible. In general, the higher your share of costs, the lower your monthly premiums will be.

Bronze plans have the lowest premium costs and the highest out-of-pocket share, while platinum plans have the highest premiums and lowest out-of-pocket expense. The type of plan that is best for you depends on your medical needs and budget.

Lowering Costs With ACA Subsidies in Florida

Since costs are often a major factor in choosing a plan, keep in mind that there is help available to most Florida residents. You may not know that in 2020, 95% of Florida residents qualified for premium tax credits that reduced their monthly premiums, and 66% were eligible for cost-sharing that reduced out-of-pocket expenses.7

How much does health insurance cost per month in Florida?

Prices for ACA health plans vary depending on your age, location, tobacco use, plan category, and whether the plan covers dependents.8 The average price for a Florida ACA plan without a tax subsidy in 2021 is $597. With a tax subsidy, it’s $98.9

Who qualifies for premium tax credits?10

Families earning between 100% and 400% of the Federal Poverty Level (FPL) can lower or cover the cost of premiums either in direct payment to the health insurance provider or expensed in their annual tax return. In 2021, eligible income is from $12,760 to $51,040 for an individual and from $26,200 to $104,800 for a family of four.

Premium tax credits may be applied toward any metal level ACA plan.

Ready to see how much you could lower your health insurance premiums? Visit the HealthMarkets shopping experience and we’ll help you calculate.

Who qualifies for cost-sharing reduction?10

Families earning between 100% and 250% of the FPL can have the health insurance provider lower or cover more out-of-pocket costs when health services are received. In 2021, that means individuals earning between $12,760 to $31,900 per year. For a family of four, that would be between $26,200 and $65,500.

Cost sharing reductions are available only to qualified people who purchase silver plans.

Short-Term Health Insurance Plans in Florida

Affordable Care Act plans are valuable for long-term coverage. But what if you only need health insurance for a limited time to tide you over until employer or Medicare coverage begins? Or until the start of the ACA’s Open Enrollment Period? Or for any other reason you may need an affordable temporary plan? That’s why short-term health insurance options are available.

In Florida, you can have short-term coverage for a little as one month, or up to 36 months.11 The benefits of short term plans are that you can apply anytime during the year, you could have coverage as soon as 24 hours after applying, and you can cancel your plan at any time.12

However, short-term plans are not ACA compliant, so they do not have to include the law’s ten essential benefits such as prescription drugs, maternity care, and no-cost preventive services. These plans also do not have the pre-existing condition protections of ACA plans.13

Interested in short-term health insurance in Florida? HealthMarkets can help you shop, compare, and apply for a short-term plan now.

Health Coverage Options for Low-Income Floridians

Who is eligible for Medicaid in Florida?

To qualify for Florida Medicaid health services, you must be a resident of Florida, a U.S. national, citizen, permanent resident, or legal alien. Individual income must not exceed $16,971 per year. A family of 4 must not exceed $34,846 per year. In addition, you must also be at least one of the following:14

- Pregnant

- Responsible for a child 18 years of age or younger

- Blind

- Have a disability or a family member in your household with a disability

- Be 65 years of age or older

For more information, visit the Florida Medicaid website.

Health Insurance for Florida’s Low-Income Children

Florida KidCare is a low-cost health insurance program for children up to age 18. Eligibility and costs are determined by income and household size.15 To apply, visit the KidCare website.

Health Insurance Florida Help from HealthMarkets

If you’re ready to purchase a health insurance plan in Florida, or are just curious about what’s available, shop and compare plans now. The HealthMarkets FitScore® can take your preferences and find plans that match—the higher the FitScore, the closer the match. Shop, compare, and apply all in one place.