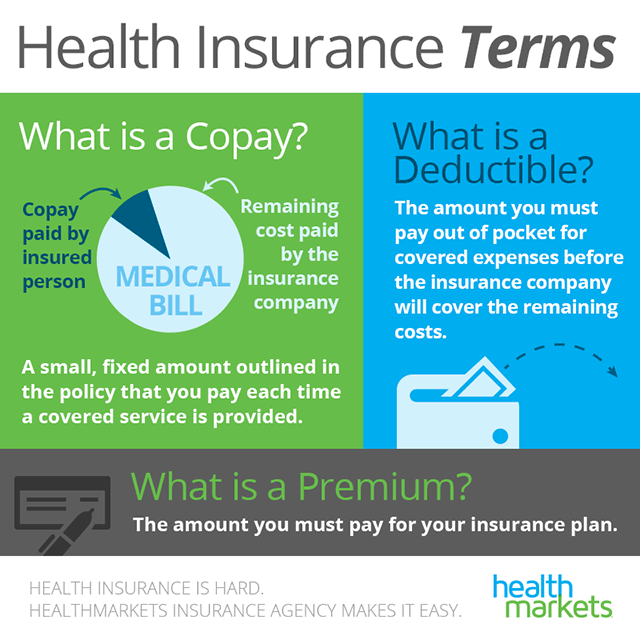

Your copayment, or copay, is a fixed amount that you pay in addition to your premium for covered healthcare services including doctor’s visits, specialist visits, or prescription drugs. Once your copay is paid, your health insurance provider covers the remaining cost of the service. The amount of your copay can vary depending on the type of healthcare service.

Your deductible is the amount you owe for covered health care services before your health insurance or plan begins to pay. For example, assume you have to go in for a covered procedure that costs $3,000. Your deductible is $1,000. In this scenario, your plan won’t pay anything until you’ve met your $1,000 deductible for this covered procedure. The deductible may not apply to all services.

With coinsurance, you and your health insurance company each pay for a percentage of your health insurance costs once you meet your deductible. A common example is an 80/20 coinsurance plan. For example, let’s say your health insurance plan’s allowed amount for an office visit is $100 and you’ve met your deductible. Your coinsurance amount of 20% would be $20 and the health insurance plan pays the rest of the allowed amount. Other common splits include 70/30 and 90/10.

What Determines Premium Rates?

The amount you pay in premiums can be affected by a number of factors. Even if two individuals are enrolled in the same health plan, they may still pay different premiums rates. Your health and lifestyle can be factored into the amount you pay for health insurance.

The factors that can affect your premium rates include:

- Your Tobacco Use: Those who currently use cigarettes, chewing tobacco, or snuff can risk being charged a high premium rate. You may even have to pay a higher premium if you’ve recently quit using tobacco. This is due to the risk of cancer and illnesses that result from frequent use of tobacco products.

- Your Age: Usually the younger you are, the lower your premium. Younger people don’t go to the doctor as often, and normally don’t have as many health concerns as older people.

- Family Size: Depending on whether you’re buying health insurance for yourself or for your spouse and/or children, you may be charged a higher premium the more people are added to your plan.

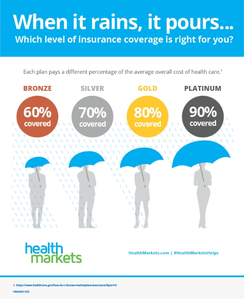

- Plan Category: Each Affordable Care Act (ACA) plan category, or metal level, is designed to pay a different percentage of you healthcare costs. Generally, the higher the metal level, the higher the premium.

- Your Location: For factors including climate or a lack of healthy food options, Americans who live in the same area may have the same health risks as each other. Because of this, health insurance companies consider where you live when determining your premium. Insurance providers may also only be available in certain areas, so lower-premium options may not be available and pricing may be higher.

Metal Levels Determine Your Premiums and Coverage for ACA Plans

To be clear about what you can control, you can choose how much you pay in premiums based on your selection (the plan’s level of coverage) or “metal level,” if you’re considering ACA-qualified health insurance plans.

Essentially, if you are willing to pay a higher premium rate, you can pay lower out-of-pocket costs when you go to get health care (and if you want to pay less in premiums, you can expect to pay higher out-of-pocket costs).