The Top 5 Things You Need to Know About Obamacare

The Affordable Care Act (ACA) affects all of us, so it’s important to understand some key components. The law, also known as “Obamacare” and “The Patient Protection and Affordable Care Act,” was created to give more Americans access to quality healthcare.¹,²

President Barack Obama signed the ACA into law in 2010. Since then, some of the law’s provisions have continued to change and evolve. The law includes:¹,²

- A guaranteed-issue provision, meaning you cannot be denied health insurance for pre-existing conditions.

- Subsidies to assist low-income Americans in purchasing health insurance coverage.

- A provision that all qualified health insurance plans must offer free preventive care.

Here are the top five things you need to know about the ACA.

1. The 10 Essential Health Benefits³

Every ACA plan is required to cover 10 essential healthcare services. Many plans offer additional benefits, but you can count on these 10 benefits in all plans:

- Prescription drugs

- Pediatric services

- Preventive and wellness services and chronic disease management

- Emergency services

- Hospitalization

- Mental health and addiction services

- Pregnancy, maternity, and newborn care

- Ambulatory patient services

- Laboratory services

- Rehabilitative and habilitative services and devices

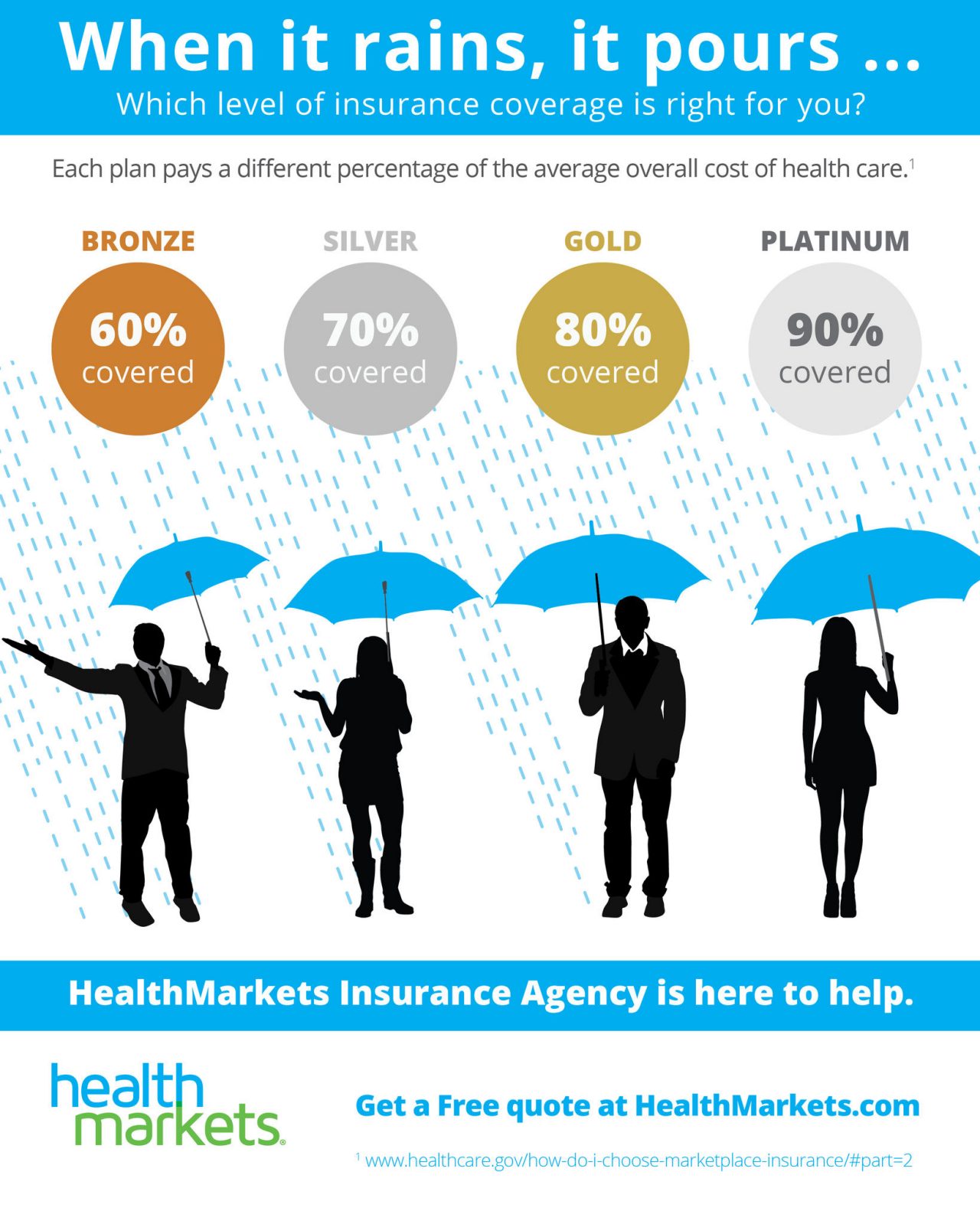

2. Tier Coverage4

There are four levels, or [glossary ignore=”true”]tiers[/glossary], of coverage that offer the 10 essential health benefits: Bronze, Silver, Gold, and Platinum. The tiers vary regarding prescription drugs, specialty care, treatments, and other covered medical expenses.

The main difference is how you and your insurance company split the out-of-pocket costs. Bronze plans have the lowest monthly premium but the highest out-of-pocket expenses. Platinum plans have the highest up-front premiums but the lowest out-of-pocket costs.

- Bronze: 60% covered by your health insurance provider; 40% covered by you

- Silver: 70% covered by your health insurance provider; 30% covered by you

- Gold: 80% covered by your health insurance provider; 20% covered by you

- Platinum: 90% covered by your health insurance provider; 10% covered by you

There is also another level: Catastrophic health insurance plans. This coverage is available for people under 30 and those with hardship exemptions. These plans are designed to provide coverage only in worst-case scenarios, where medical costs are often very high.5

Beyond premium rates and cost-sharing, there are other variables to consider, such as plan benefits, provider networks, the insurance company, and subsidy availability.

3. Tax Subsidies

If you’re worried about the cost of health insurance, you may be in luck. Depending on your annual income, you could receive financial assistance—in the form of a tax subsidy—to pay for some of your premium. In 2020, 86% of people with ACA plans purchased from a federal or state exchange received this subsidy.6

Those making between 100% and 400% of the federal poverty level (FPL) receive a tax credit. (In 2021, that’s $12,760 to $51,040 for individuals and $26,200 to $104,800 for a family of four).7 Use the Subsidy Calculator here to see if you qualify.

Your Income Level7 |

Expected Contribution7 |

|

|---|---|---|

100% – 133% of the federal poverty level |

2.07% of your income |

|

133% – 150% of the federal poverty level |

3.10% – 4.14% of your income |

|

150% – 200% of the federal poverty level |

4.14% – 6.52% of your income |

|

200% – 250% of the federal poverty level |

6.52% – 8.33% of your income |

|

250% – 300% of the federal poverty level |

8.33% – 9.83% of your income |

|

300% – 400% of the federal poverty level |

9.83% of your income |

4. Open Enrollment Period (OEP)8

Every fall, the Open Enrollment Period begins, allowing individuals and families to sign up for an ACA plan through a variety of options.

For most states, the Open Enrollment Period is November 1 to December 15. Sometimes, states with their own exchanges choose to extend the enrollment period for their residents. View your state’s Open Enrollment Period.

An important detail: In some states, residents who don’t obtain health coverage must pay a tax penalty.9

5. Special Enrollment Period (SEP)10

A Special Enrollment Period (SEP) allows people with a “qualifying life event” to enroll in an individual health insurance plan outside of the Open Enrollment Period (OEP). The SEP only lasts for 60 days, beginning on the date of the qualifying event.

Qualifying life events can include:

- Non-renewal of your insurance coverage

- Change in family size: This includes marriage, divorce, child birth, adoption, or death.

- Job change: An interruption in health coverage due to job loss. In this case, you may apply for new coverage up to 60 days before your insurance is terminated.

- Change in citizenship: Becoming an American citizen, or obtaining national or legal status.

- Government error: Your coverage is changed by an error caused by the Health Insurance Exchange or the Department of Health and Human Services.

- New Address: You move to a new state or county.

HealthMarkets Makes Finding an ACA Plan Easy

HealthMarkets is here to help you find the best price available on the plans we offer. Use the HealthMarkets FitScore™ to find the ACA plans that best fit your needs. Compare plans now. The plans with the highest FitScore are the most ideal match for your needs. Not sure if an ACA plan is right for you? Let us help you find coverage, even if your best option doesn’t include plans we offer. Call us at (888) 510-6306.

1. HealthCare.gov. Retrieved from https://www.healthcare.gov/glossary/patient-protection-and-affordable-care-act/

2. HealthCare.gov. Retrieved from https://www.healthcare.gov/health-care-law-protections/

3. HealthCare.gov. Retrieved from https://www.healthcare.gov/coverage/what-marketplace-plans-cover/

4. HealthCare.gov. Retrieved from https://www.healthcare.gov/choose-a-plan/plans-categories/

5. HealthCare.gov. Retrieved from https://www.healthcare.gov/choose-a-plan/catastrophic-health-plans/

6. Kaiser Family Foundation. 2020. Retrieved from https://www.kff.org/other/state-indicator/effectuated-marketplace-enrollment-and-financial-assistance/

7. Kaiser Family Foundation. October 30, 2020. Retrieved from https://www.kff.org/health-reform/issue-brief/explaining-health-care-reform-questions-about-health-insurance-subsidies/

8. HealthCare.gov. Retrieved from https://www.healthcare.gov/quick-guide/dates-and-deadlines/

9. HealthCare.gov. Retrieved from https://www.healthcare.gov/fees/fee-for-not-being-covered/

10. HealthCare.gov. Retrieved from https://www.healthcare.gov/coverage-outside-open-enrollment/special-enrollment-period/