Choosing Medicare coverage can feel overwhelming, especially with so many Medicare Advantage plans available.

During open enrollment…

- It can feel like Medicare Advantage ads are everywhere on TV, radio, YouTube, social media, and even in your mailbox.

- With so much information coming at you at once, it is not always clear how these plans work or how they differ from Original Medicare. Sound familiar?

Understanding the basics can help you compare your choices and find coverage that fits your health care and cost preferences.

Medicare Advantage plans explained

Medicare Advantage plans (also called Medicare Part C) are offered by private insurance companies that contract with Medicare.1

Because they are offered by private insurance companies, Medicare Advantage plans can also include additional benefits and coverage that are not offered by Original Medicare, such as prescription drug coverage.2

This flexibility means there’s a lot to understand when comparing Medicare Advantage options.

If you already know what you’re looking for, you can start shopping now.

- If you’re unsure of what kind of Medicare Advantage plan may be right for you, read on for more information.

Medicare Advantage plans & Original Medicare: What’s the difference?

Here’s a quick look at how Medicare Advantage plans compare to Original Medicare so you can understand what each type of coverage includes.3

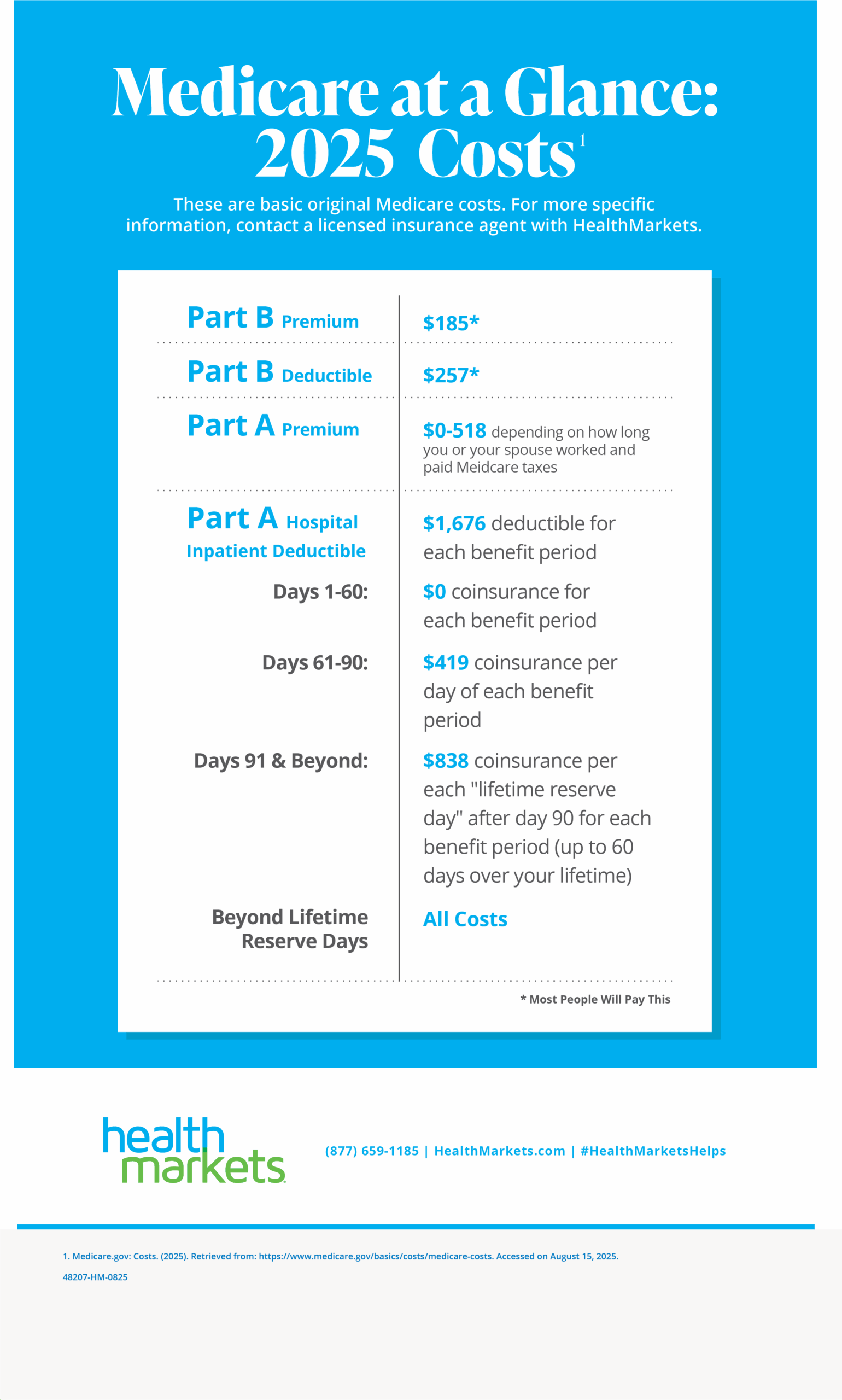

Premiums

Original Medicare beneficiaries pay a premium for Part B and may also pay a Part A premium if they have not paid Medicare taxes for at least 10 years.

Medicare Advantage plans require you to continue paying your Part A premium (if applicable) and your Part B premium. Some Medicare Advantage plans may also charge an additional monthly premium. Premium amounts vary by plan and location.

Out-of-pocket expenses

Original Medicare beneficiaries pay a deductible and typically 20 percent coinsurance for most Part B services.

Medicare Advantage plans have deductibles, but many use copays instead of coinsurance. Costs for deductibles, copays, or coinsurance vary by plan.

Out-of-pocket limit

Original Medicare does not include an annual out-of-pocket cap, which means there is no limit to how much you could pay for covered services.

All Medicare Advantage plans must include an out-of-pocket limit. Once you reach your plan’s limit for the year, you generally will not pay for covered services for the rest of the year. The specific out-of-pocket limit varies by plan and can change annually.

Choice of physician

Original Medicare generally allows you to visit any doctor or hospital in the United States that accepts Medicare.

Medicare Advantage HMO plans typically require you to use a network of contracted physicians and may require you to choose a Primary Care Physician and get referrals for specialists.

Medicare Advantage PPO plans allow you to see out-of-network providers, but you may pay more.

Medicare Supplement Insurance

Beneficiaries with Original Medicare may choose to purchase a Medigap policy to help with out-of-pocket costs.

Medicare Advantage: You cannot buy Medigap while enrolled in a Medicare Advantage plan.

Prescription drug coverage

Original Medicare beneficiaries must purchase a separate Prescription Drug Plan if they want drug coverage. This is known as Medicare Part D.

Many Medicare Advantage plans include prescription drug coverage. These are called Medicare Advantage Prescription Drug plans. Part D plans have a federally set out-of-pocket limit for 2026 of $2,100, and plan deductibles may vary by plan.4

If you enroll in a Medicare Advantage plan without prescription drug coverage, you may not be able to join a separate Prescription Drug Plan without being disenrolled from your Medicare Advantage plan.

Dental, vision & hearing

Original Medicare only covers medically necessary services and does not include routine dental, vision, or hearing benefits.

Some Medicare Advantage plans may include additional benefits such as dental, vision, and hearing. Availability varies by plan and location.

Compare Medicare Advantage & Original Medicare

This table will help you easily identify the main differences between Original Medicare and Medicare Advantage plans: